MILLIONS of workers are set to get a pay rise from tomorrow thanks to a government change.

The amount of tax people pay will be slashed after changes are made to the way National Insurance is paid.

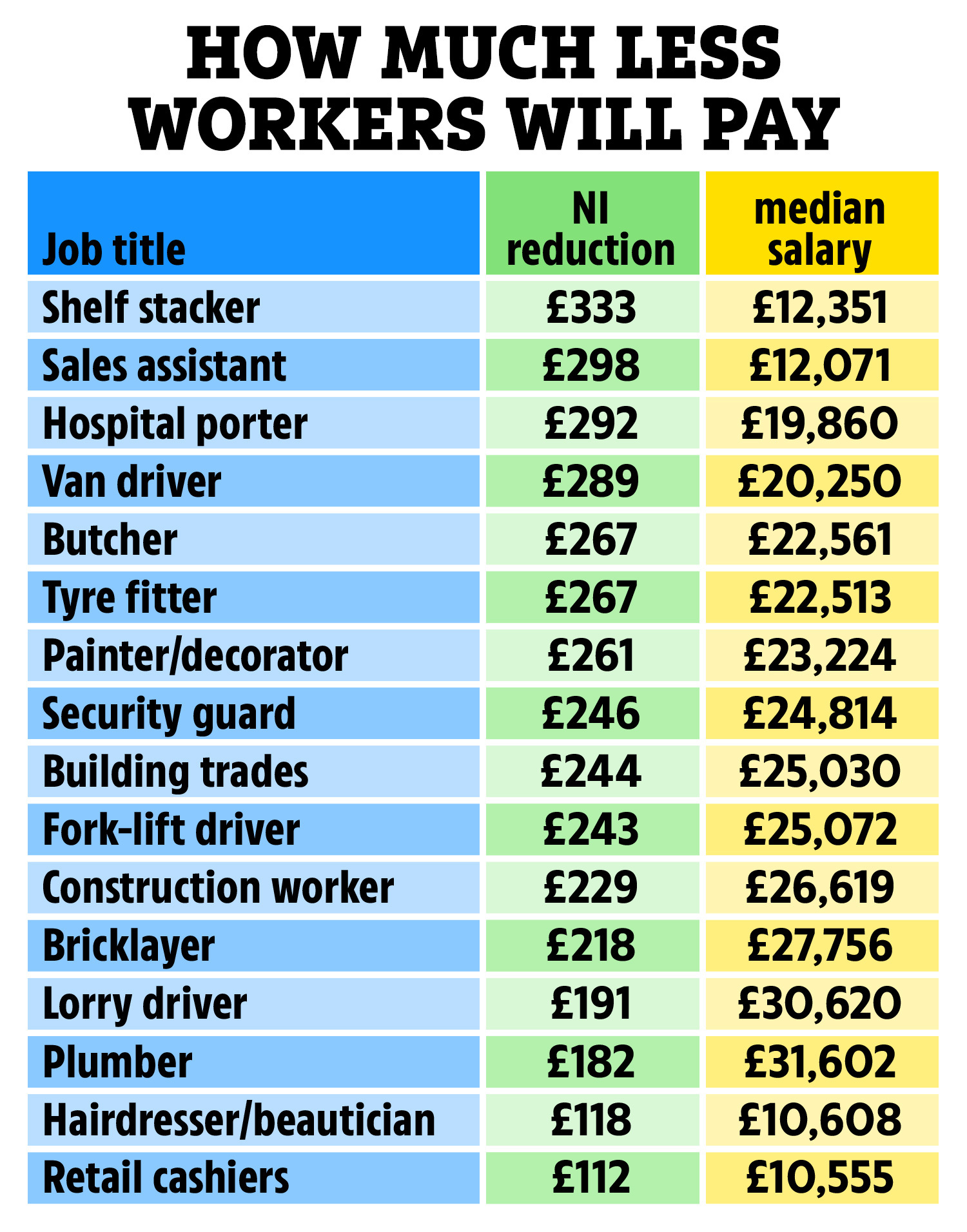

Workers are getting a pay rise from a tax change

The threshold for making National Insurance contributions (NICs) will rise from £9,500 to £12,570 from July 6.

Now, SE can exclusively reveal how much more money a range of workers can expect to see in their bank accounts this year.

The data reveals shelf stackers will see the biggest drop in National Insurance Contributions (NICs), with an extra £333 heading into their bank accounts this year.

Sales assistants are next, with £292 and then hospital porters with £292.

The statistics are based on median salaries for each occupation.

If your job is not included in the list, you can try the government’s handy online tool yourself on the government’s website to get an estimate of how much less NICs you’ll pay after the change.

It comes as energy bills and fuel and food costs soar for many, leaving millions of households out of pocket.

Prime Minister Boris Johnson said on Sunday the changes will save 30million workers as much as £330 a year.

And 2.2million people will be lifted out of paying any National Insurance altogether.

The change was first announced in March by chancellor Rishi Sunak and comes with prices rising at a rate of 9.1%, which could worsen to 11% according to experts.

How much workers can expect extra in their pay each year after paying less NICs

How much workers can expect extra in their pay each year after paying less NICs

This has seen everyday items like food and petrol cost much more than they did this time last year.

On top of the NICs reduction, the government has also announced a package of support worth up to £1,500 for the most hard-up households.

Steven Cameron, pensions director at Aegon, said despite the government freezing most tax thresholds until 2026 and the employee rate of NI increasing in April to 13.25%, tomorrow’s news was positive.

“The lower threshold of earnings on which employees pay National Insurance is increasing which for most will mean a boost in take-home pay of around £30 per month.

He added: “In further good news, those no longer paying NICs will still receive credits towards their future state pension as long as they earn above £6,396 a year.

“While this will be welcomed by those individuals, it does call into question the sustainability of state pension funding with today’s state pensions being paid for from the NICs of today’s workers.”

What is National Insurance?

National Insurance (NI) is a contribution workers make out of their monthly pay packet to qualify for benefits such as a state pension, sick pay or unemployment benefits.

You pay NI if you’re 16 or older and are either an employee earning above £190 a week or are self-employed and making a profit of £6,725 or more a year.

Workers currently pay 13.25% on earnings between £9,564 and £50,268 and a further 3.25% is paid on wages over that.

But you don’t need to pay for NI after reaching state pension age, which is currently 66, but will rise to 67 by 2028.

National Insurance is not the same as income tax, and you pay this separately on your earnings too.