A wealth manager is a financial advisor who helps high net-worth individuals and families manage their financial affairs. Their services range from basic tax and retirement planning to estate and charitable giving. In addition to these core services, a wealth manager may also provide investment advice. Depending on the company, a wealth manager's fees may be more than a typical financial advisor's. A wealth manager typically charges 3% of the total assets under management (AUM) for their clients.

Wealth managers are not financial advisors. They have a fiduciary duty and must act in the best interests of their clients. This means that they must take into account all possible factors and goals when preparing a plan to help achieve them. Expertise and experience in their field is also required for wealth managers. They must also be able to adapt their asset allocation to meet the needs of their clients.

A wealth manager is different than a financial advisor because they offer a more personalized approach. Many people with high net worth have complex financial circumstances and require a plan to guide them. A wealth manager can help anyone, no matter if they're saving for a wedding, setting up a business or protecting their retirement savings. The right wealth manager will be willing to spend time with you to fully understand your goals. Although it can take time to find the right wealth manager for you, you will be able to have a more thorough and informed approach to your finances.

You will receive more attention from a wealth manager and have access to more experts. Many licensed professionals have a bachelor's or grad degree. Additionally, the right advisor will have a fiduciary responsibility to act in the best interests of their clients.

A wealth manager can be an expert in all areas of financial matters including investments, tax and estate planning and charitable giving. They can work with a wealth of different types of clients, including the rich and the poor, and their services can be tailored to suit your individual needs. Wealth managers may also be certified as money coaches and credit counselors.

A financial advisor, on the other hand, is a financial planner who works with a broader group of clients, including middle-class people. Rates for financial advisors can vary depending on your financial situation. They may also charge flat fees for their services. A financial advisor can guide you in reaching your financial goals, for a very small fee.

A financial advisor will meet with your once a calendar year to discuss your financial goals. The annual review of your wealth plan is a good opportunity to ask questions and share important information. Make sure you do a background search on the FINRA site before hiring a financial consultant. Also, request references. You can make a wise investment in your future by contacting a trusted advisor.

FAQ

How can rich people earn passive income?

There are two ways you can make money online. Another way is to make great products (or service) that people love. This is called earning money.

You can also find ways to add value to others, without having to spend your time creating products. This is known as "passive income".

Let's suppose you have an app company. Your job is to develop apps. But instead of selling the apps to users directly, you decide that they should be given away for free. It's a great model, as it doesn't depend on users paying. Instead, your advertising revenue will be your main source.

You might charge your customers monthly fees to help you sustain yourself as you build your business.

This is how most successful internet entrepreneurs earn money today. Instead of making things, they focus on creating value for others.

What is the easiest way to make passive income?

There are many online ways to make money. Most of them take more time and effort than what you might expect. How do you find a way to earn more money?

The solution is to find what you enjoy, blogging, writing or selling. Find a way to monetize this passion.

For example, let's say you enjoy creating blog posts. Your blog will provide useful information on topics relevant to your niche. Then, when readers click on links within those articles, sign them up for emails or follow you on social media sites.

This is called affiliate marketing, and there are plenty of resources to help you get started. For example, here's a list of 101 Affiliate Marketing Tools, Tips & Resources.

You could also consider starting a blog as another form of passive income. Once again, you'll need to find a topic you enjoy teaching about. Once you have established your website, you can make it a monetizable resource by selling ebooks, courses, and videos.

There are many online ways to make money, but the easiest are often the best. You can make money online by building websites and blogs that offer useful information.

Once your website is built, you can promote it via social media sites such as Facebook, Twitter, LinkedIn and Pinterest. This is known as content marketing and it's a great way to drive traffic back to your site.

How to build a passive stream of income?

You must understand why people buy the things they do in order to generate consistent earnings from a single source.

Understanding their needs and wants is key. This requires you to be able connect with people and make sales to them.

The next step is to learn how to convert leads in to sales. Finally, you must master customer service so you can retain happy clients.

This is something you may not realize, but every product or service needs a buyer. And if you know who that buyer is, you can design your entire business around serving him/her.

A lot of work is required to become a millionaire. It takes even more work to become a billionaire. Why? To become a millionaire you must first be a thousandaire.

Finally, you can become a millionaire. And finally, you have to become a billionaire. It is the same for becoming a billionaire.

So how does someone become a billionaire? It starts by being a millionaire. All you have to do in order achieve this is to make money.

However, before you can earn money, you need to get started. Let's take a look at how we can get started.

What's the difference between passive income vs active income?

Passive income can be defined as a way to make passive income without any work. Active income requires work and effort.

Active income is when you create value for someone else. When you earn money because you provide a service or product that someone wants. You could sell products online, write an ebook, create a website or advertise your business.

Passive income allows you to be more productive while making money. However, most people don't like working for themselves. People choose to work for passive income, and so they invest their time and effort.

Problem is, passive income won't last forever. If you wait too long before you start to earn passive income, it's possible that you will run out.

It is possible to burn out if your passive income efforts are too intense. It is best to get started right away. If you wait until later to start building passive income, you'll probably miss out on opportunities to maximize your earnings potential.

There are three types passive income streams.

-

Business opportunities include opening a franchise, creating a blog or freelancer, as well as renting out property like real estate.

-

Investments - These include stocks, bonds and mutual funds as well ETFs.

-

Real Estate includes flipping houses, purchasing land and renting properties.

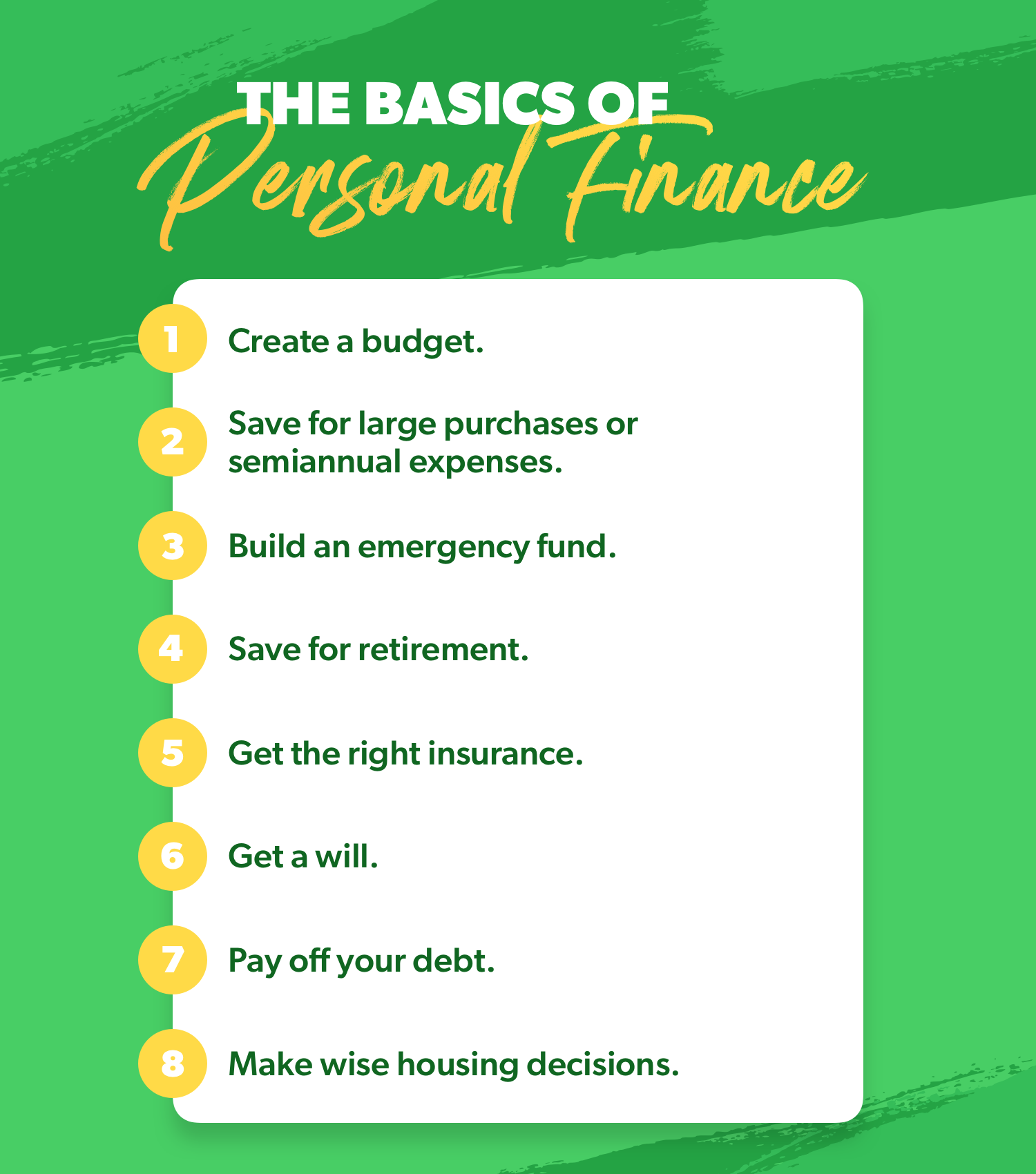

Why is personal financial planning important?

A key skill to any success is personal financial management. In a world of tight money, we are often faced with difficult decisions about how much to spend.

Why then do we keep putting off saving money. What is the best thing to do with our time and energy?

Yes and no. Yes, most people feel guilty saving money. Yes, but the more you make, the more you can invest.

You'll always be able justify spending your money wisely if you keep your eyes on the bigger picture.

To become financially successful, you need to learn to control your emotions. Focusing on the negative aspects in your life will make it difficult to think positive thoughts.

You may also have unrealistic expectations about how much money you will eventually accumulate. You don't know how to properly manage your finances.

Once you have mastered these skills you will be ready for the next step, learning how budgeting works.

Budgeting is the act of setting aside a portion of your income each month towards future expenses. Planning will help you avoid unnecessary purchases and make sure you have enough money to pay your bills.

Once you have mastered the art of allocating your resources efficiently, you can look forward towards a brighter financial tomorrow.

What is the limit of debt?

There is no such thing as too much cash. Spending more than you earn will eventually lead to cash shortages. Savings take time to grow. When you run out of money, reduce your spending.

But how much can you afford? Although there's no exact number that will work for everyone, it is a good rule to aim to live within 10%. You won't run out of money even after years spent saving.

This means that, if you have $10,000 in a year, you shouldn’t spend more monthly than $1,000. You should not spend more than $2,000 a month if you have $20,000 in annual income. For $50,000 you can spend no more than $5,000 each month.

It is important to get rid of debts as soon as possible. This includes student loans and credit card bills. When these are paid off you'll have money left to save.

You should consider where you plan to put your excess income. If the stock market drops, your money could be lost if you put it towards bonds or stocks. But if you choose to put it into a savings account, you can expect interest to compound over time.

Let's take, for example, $100 per week that you have set aside to save. Over five years, that would add up to $500. Over six years, that would amount to $1,000. You would have $3,000 in your bank account within eight years. It would take you close to $13,000 to save by the time that you reach ten.

You'll have almost $40,000 sitting in your savings account at the end of fifteen years. This is quite remarkable. You would earn interest if the same amount had been invested in the stock exchange during the same period. Instead of $40,000 in savings, you would have more than 57,000.

It's crucial to learn how you can manage your finances effectively. Otherwise, you might wind up with far more money than you planned.

Statistics

- Shares of Six Flags Entertainment Corp. dove 4.7% in premarket trading Thursday, after the theme park operator reported third-quarter profit and r... (marketwatch.com)

- Etsy boasted about 96 million active buyers and grossed over $13.5 billion in merchandise sales in 2021, according to data from Statista. (nerdwallet.com)

- As mortgage rates dip below 7%, ‘millennials should jump at a 6% mortgage like bears grabbing for honey' New homeowners and renters bear the brunt of October inflation — they're cutting back on eating out, entertainment and vacations to beat rising costs (marketwatch.com)

- 4 in 5 Americans (80%) say they put off financial decisions, and 35% of those delaying those decisions say it's because they feel overwhelmed at the thought of them. (nerdwallet.com)

- These websites say they will pay you up to 92% of the card's value. (nerdwallet.com)

External Links

How To

How to make money online

It is much easier to make money online than it was 10 years ago. The way you invest your money is also changing. There are many ways that you can make passive income. But, they all require a large initial investment. Some methods are easier than other. Before you start investing your hard-earned money in any endeavor, you must consider these important points.

-

Find out what kind of investor you are. If you're looking to make quick bucks, you might find yourself attracted to programs like PTC sites (Pay per click), where you get paid for simply clicking ads. If you're looking for long-term earning potential, affiliate marketing might be a good option.

-

Do your research. Before you make a commitment to any program, do your research. Review, testimonials and past performance records are all good places to start. You don’t want to spend your time and energy on something that doesn’t work.

-

Start small. Do not jump into a large project. Instead, you should start by building something small. This will help you learn the ropes and determine whether this type of business is right for you. When you feel confident, expand your efforts and take on bigger projects.

-

Get started now! It's never too early to begin making money online. Even if a long-term employee, there's still time to build up a profitable portfolio of niche websites. All you need are a great idea and some dedication. Get started today and get involved!